Even though Park-Ohio (currently trading at $20.60 per share) has gained 12.8% over the last six months, it has lagged the S&P 500’s 26.5% return during that period. This might have investors contemplating their next move.

Is there a buying opportunity in Park-Ohio, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Is Park-Ohio Not Exciting?

We're swiping left on Park-Ohio for now. Here are three reasons we avoid PKOH and a stock we'd rather own.

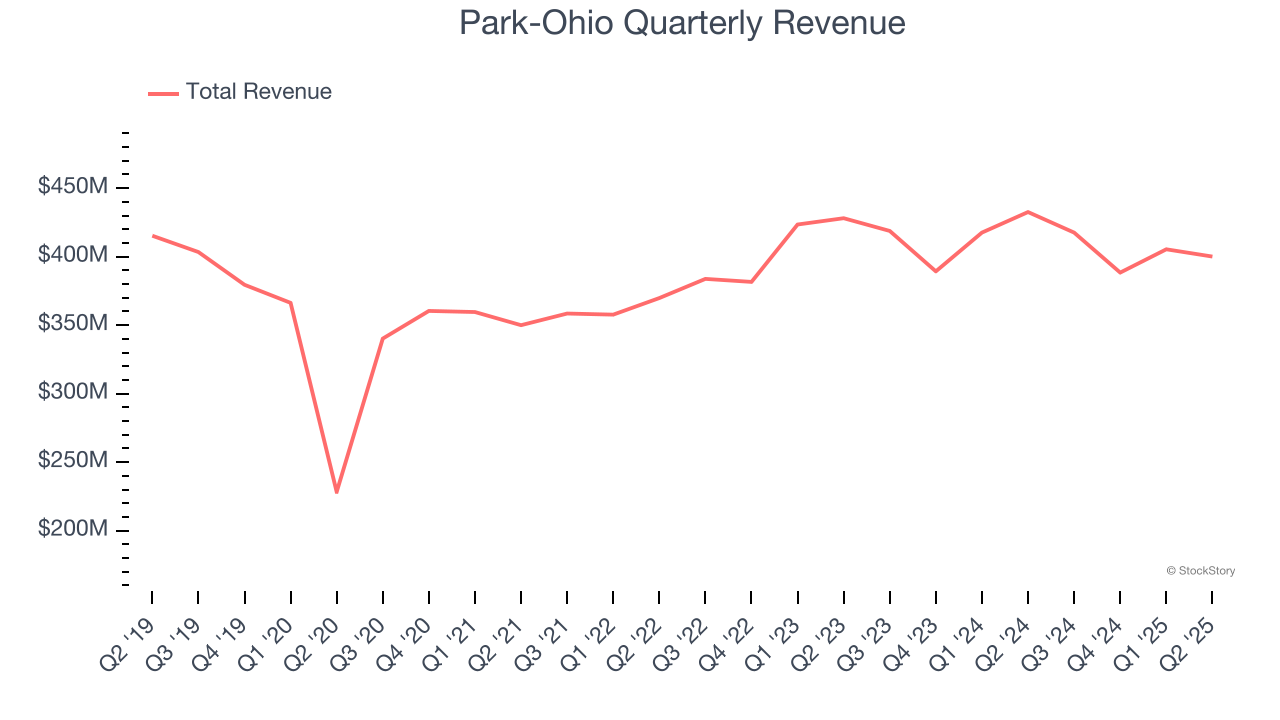

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Park-Ohio’s 3.2% annualized revenue growth over the last five years was sluggish. This was below our standard for the industrials sector.

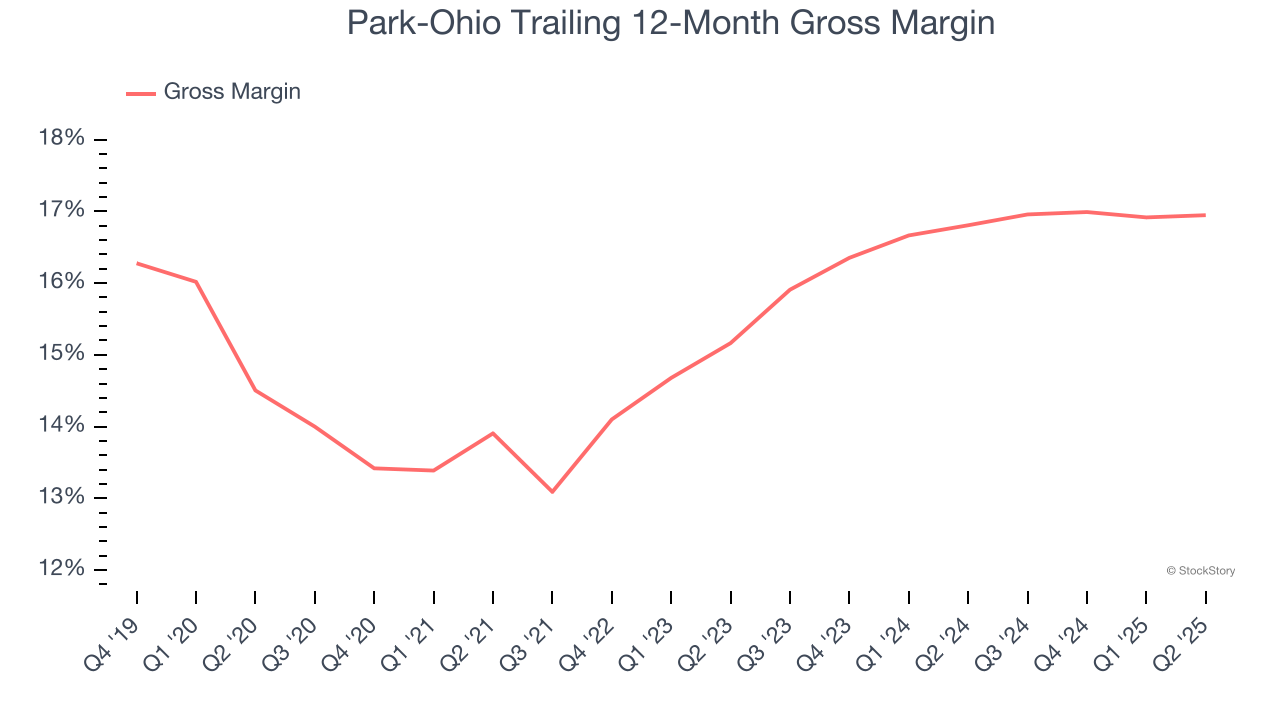

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

Park-Ohio has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 15.4% gross margin over the last five years. Said differently, Park-Ohio had to pay a chunky $84.59 to its suppliers for every $100 in revenue.

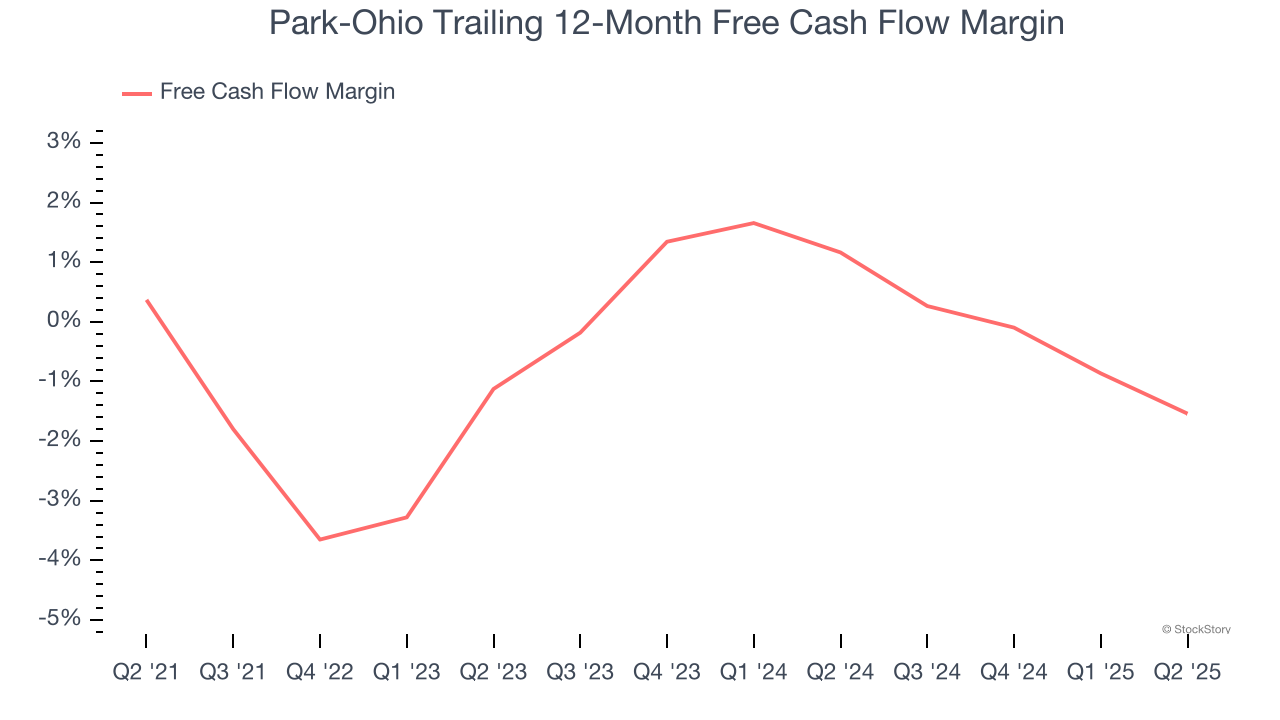

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Park-Ohio’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.1%, meaning it lit $1.12 of cash on fire for every $100 in revenue.

Final Judgment

Park-Ohio isn’t a terrible business, but it isn’t one of our picks. With its shares trailing the market in recent months, the stock trades at 6.5× forward P/E (or $20.60 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.